There are several provisions in the insurance laws that prevent consumers from realizing all the benefits of UBI. FSCO’s Bulletin No. A-16/16 imposes restrictions on the ways in which consumers can be enrolled in UBI and the ways in which insurers can use the data collected through the UBI device.

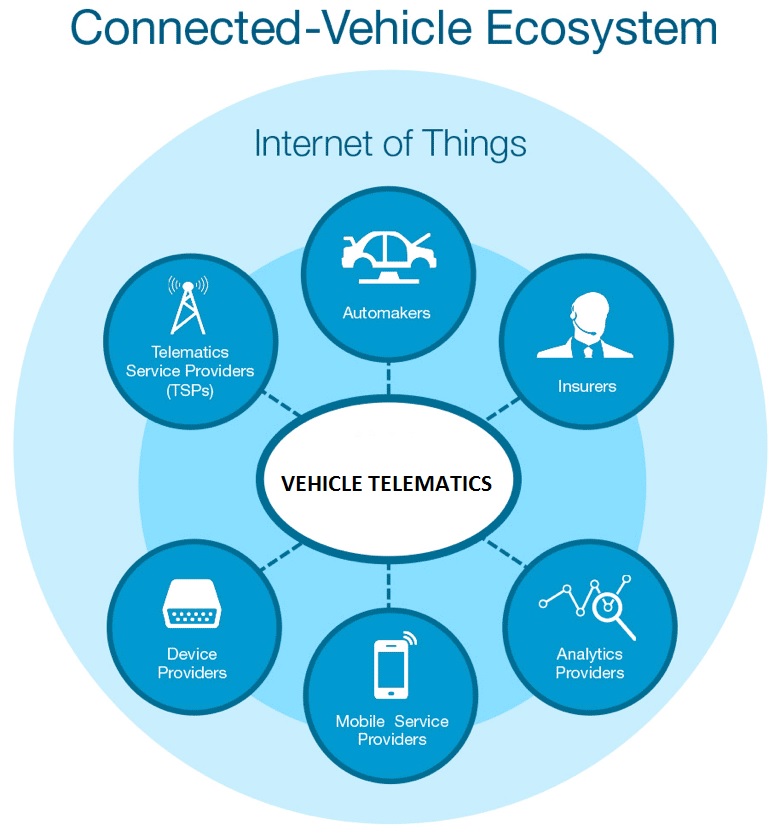

Consumers are driving the demand for easy, flexible and tailored products with dynamic pricing being offered in sectors as diverse as entertainment, retail and banking. UBI provides an opportunity for insurers to customize insurance to their customers’ unique driving behaviours and vehicle usage patterns. UBI typically consists of a device installed in a customer’s vehicle or an app downloaded on a smartphone that allows insurers to track distance driven and driving behaviours, and to collate this information to determine a price for insurance. UBI provides insurers the opportunity to engage more frequently and meaningfully with customers. It gives customers access to information about their driving performance. And it provides them with more control over their auto insurance costs because their usage patterns, mileage and driving behaviour can directly influence the price. UBI also generates significant societal benefits by promoting safer driving habits.

UBI has the potential to more accurately price risk. For many customers, it could result in insurance that costs less than that priced through traditional means. With the current rules, however, an insurer can only use UBI to offer a discount on the price set through its traditional pricing formula. The insurer cannot use the data regarding the individual’s actual driving habits to determine the premium price.

RECOMMENDATION:

IBC recommends that FSCO allow insurers to provide consumers the option to select UBI to determine the price of their auto insurance.

A popular UBI product comes from the insurer Metromile, which sets premium price solely on the data collected through the device.

Based on the premise that the number one risk to drivers is how often they drive, Metromile offers a product for lowmileage drivers. In the U.S., Metromile estimates that 65% of households drive less than 12,000 miles per year and might benefit from the program. The product is a per-mile rate for every mile driven applied to a low monthly base price. If individuals drive fewer miles, they pay less for insurance. Conversely, if they drive more, they pay more for insurance.

A 2017 Willis Towers Watson survey examined how the spread of in-car technologies and connected cars is influencing U.S. consumers’ buying behaviours and attitudes toward UBI.