Changes are occurring at a rapid rate in today’s auto insurance world.

From the InsurTech boom to semi-autonomous car technology — there have been many advances in the once slow-moving industry.

Most notable are the shifts in drivers’ road habits that are encouraging auto insurers to change their traditional ways. The way people drive has led to new insurance models, more coverage options and greater integration of technology.

The National Highway Traffic Safety Administration released estimates that traffic fatalities were up 10.4 percent in the first six months of 2016 over last year. While a strong economy and low gas prices result in more miles driven, there is still an increase in traffic deaths once that is accounted for. What’s causing the fatal jump?

Driver inattention on the road is increasing as motorists grow more distracted. Some states have even seen distracted driving fatalities doubling. Speeding and drunk or drowsy driving may also be contributing to the increase. Here’s how dangerous driving habits are changing the auto insurance industry right now.

“Pay how you drive” insurance models

Many insurers have implemented “Pay how you drive” models to adapt to drivers’ changing habits and the insurance telematics market is forecast to grow at a 50% compound annual growth rate by 2020. This model appears to be exactly what drivers were looking for as there are now 12 million drivers utilizing usage-based insurance.

While data has previously been used to price premiums, it has operated under generalities. A more personalized model is appealing to drivers who have previously been frustrated by auto insurers’ assumptions. In other pricing models, drivers may have a risk profile that does not accurately represent them and is based on average data for all drivers in their age group or city. With “Pay how you drive”, drivers have more control as telematics devices measure their habits.

“Pay how you drive” models can save both insurers and consumers money and many agents are choosing to recommend them for their efficiency and accuracy. Carriers can make informed decisions and determine a premium price based not only on location, age or driving record, but also on individual driving behaviors.

With UBI, drivers can be priced accurately based on their risk and that will offer a value to customers. “Pay how you drive” will help keep drivers safe by providing peace of mind and highlighting driver improvement areas. The driver can then work to improve his or her habits for a safety and cost benefit. Additional unique services can also be offered through this technology, such as vehicle diagnostics, real-time navigation and in-vehicle entertainment systems which may boost consumer satisfaction.

UBI allows insurers to understand the shifting habits of drivers to a greater degree and adjustments can be made if a driver exhibits risky behavior or develops unsafe habits. Both drivers and insurers can benefit from “Pay how you drive” insurance models.

Shared mobility coverage

With technology advancements, drivers’ behavior is shifting toward lower vehicle ownership. Habits are changing and more drivers are choosing to use ridesharing services or car share their own vehicle. Considering that cars are parked 95 percent of the time, shared mobility is sensible as it improves efficiency and can be more cost effective, especially in urban environments. Uber and Lyft offer ridesharing services while companies like Maven and Getaround allow you to rent a car per hour or put your own vehicle up for car share.

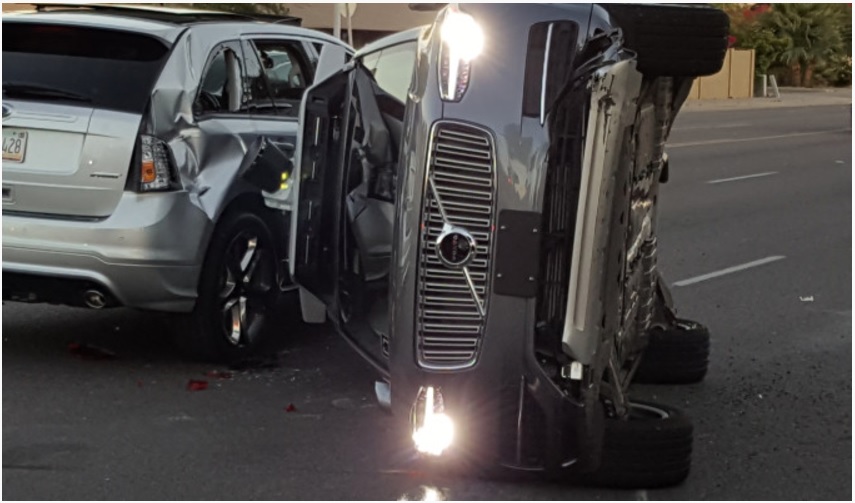

Things on the road are changing. Insurers and agents should keep up and remain aware of ways to adapt to the shifting industry. (Photo: iStock)

Drivers’ adoption of shared mobility has opened up new opportunities for insurers. Some providers have partnered directly with ridesharing and car sharing companies while others have developed their own coverage services. Berkshire Hathaway insures Getaround’s car sharing members while Geico and State Farm, among others, offer ridesharing coverage to Transportation Network Company (TNC) drivers.

Shared mobility will likely increase in future years as technology advances and drivers continue to shift away from multi-vehicle car ownership toward more efficient modes of transportation. Shared-use mobility challenges vehicle-centric underwriting as drivers may operate multiple different cars or have more drivers using their own vehicle. Insurers are adapting to these changes by offering new coverage options and creating partnerships.

Safe-driving technology

While many insurers do offer usage-based insurance programs, not all providers do yet. However, there are other safe-driving technologies available that insurers have adopted to improve drivers’ behavior behind the wheel and agents can recommend.

Many insurers have partnered with apps like CellControl or TrueMotion to help stop distracted driving by blocking incoming calls and texts when a driver is behind the wheel. Other apps like EverDrive or DrivingBuddy give drivers an overall score on trips and suggest improvement areas. They measure driving skills such as speeding, braking, acceleration and phone use. These apps can make drivers more aware of their own habits, and give them feedback to improve. Additionally, there are various hands-free devices available as well as backup cameras to help drivers operate safely on the road.

There is safe-driving technology available now that insurers and agents can recommend to build up their current customer pool. Drivers that improve their skills are less likely to get into accidents and file claims, which will cut costs for everyone involved. Insurers can also encourage independent use of these technologies, so that consumers may be more motivated to improve their skills on their own to become better drivers.

The bottom line for insurers and agents? Be Flexible.

Driving habits are changing the auto insurance industry and they will continue to do so. Auto insurers and agents may want to remain flexible and look ahead to semi-autonomous and fully autonomous vehicles as they will continue to change drivers’ habits and perhaps, make them obsolete. The car technology is coming, and while it may not be widely adopted for several years—how insurers adapt to this transportation disruption will determine the severity of its effect on the industry.

While the government recently announced their own policy and guidelines, insurers and agents should determine a roadmap to prepare for further integration of the Internet of Things. The government is working to find a balance between innovation and safety, and insurers may want to do the same within their own industry.

Some insurers are already doing so by preparing for new forms of coverage such as cybersecurity insurance for potential hacks. Others are teaming up with self-driving car makers and researchers to gain insight into the technology.

Auto insurance premiums could drop 30 percent from current levels over the next 25 years. Car insurers may not be dealing with driver negligence anymore — instead, there may be an increase in product liability claims. Risk pricing may rely predominantly on the make and model of the vehicle rather than the driver. That said, computers make mistakes, too, and there will be new risks to insure for — possible hacks, satellite failure or sensor damage. Furthermore, there will likely be an in-between transitional period where both autonomous and human-driven cars are on the roads, which will result in unique coverage needs.

Driverless cars will happen, so insurers and agents may what to remain flexible and prepare. Just don’t disregard the driving habits that are already changing the auto insurance industry today.

Read more at http://www.propertycasualty360.com/2016/10/26/how-driving-habits-are-changing-the-auto-insurance?page_all=1